The salary-day autopilot

Rees Calder · 6 May 2026 · 6 min read

The average person who donates by standing order gives four times more per year than someone who gives when the mood takes them. The standing order donors aren't richer. They're not more virtuous. They just removed a decision from the equation.

That's the entire trick. The less you have to decide, the more you give.

Here's how to set it up in about eight minutes.

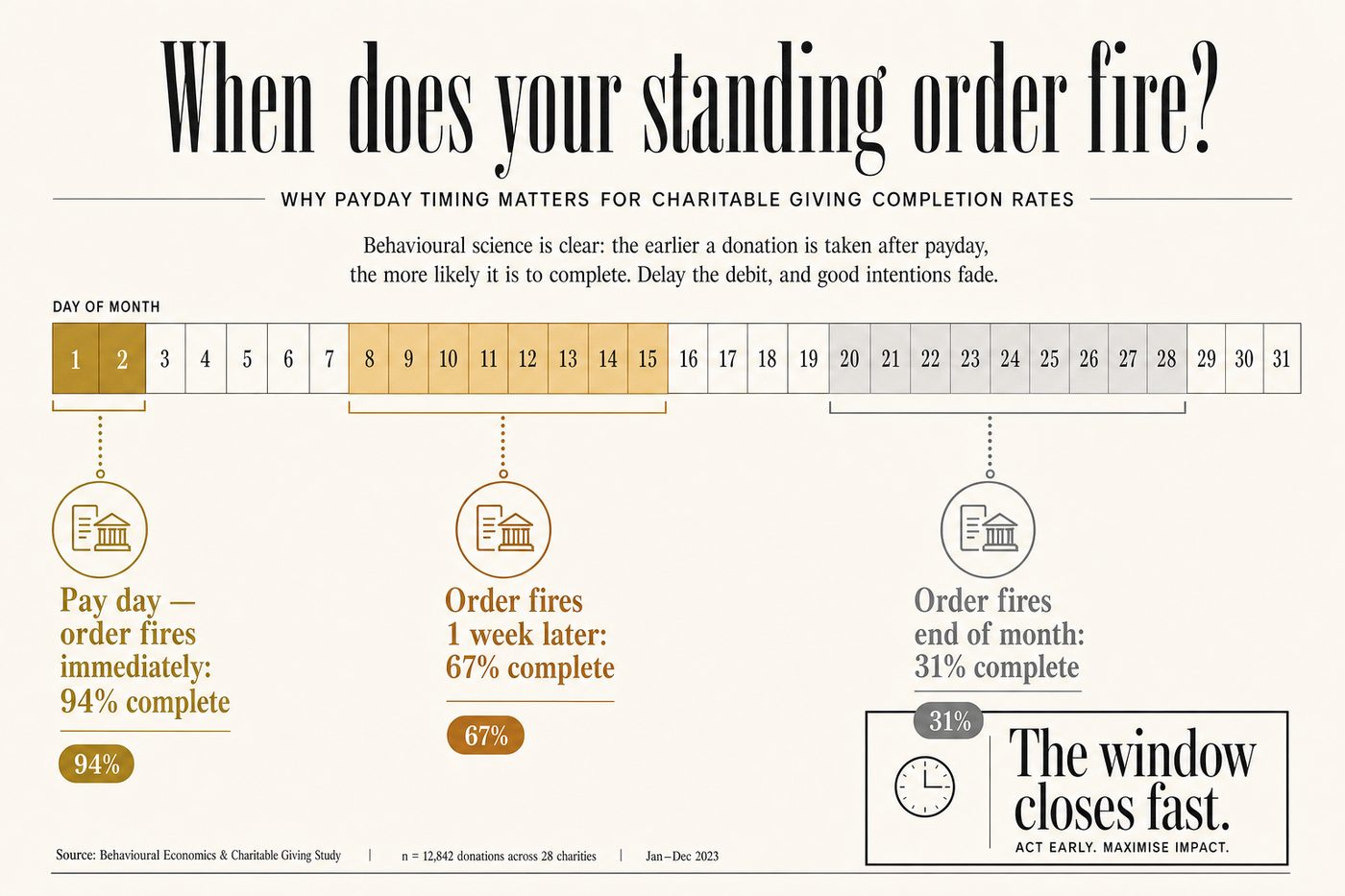

Why payday is the only trigger that works

Decision fatigue compounds badly around money. By the time payday arrives you've already made dozens of financial micro-decisions that day. By the time you get around to thinking about charity, it's three weeks later, the account looks vaguely normal, and the moment has passed. You tell yourself you'll do it next month.

The fix is to intercept the money before you categorise it as "mine." Payroll savings schemes figured this out decades ago: money you never see in your current account is money you don't miss. Same principle applies to giving.

Set your standing order to trigger on payday. The same day your salary lands. Not the next day. Not when you've paid rent. Before the money becomes "spending money" in your mental accounting, it's already gone somewhere better.

What percentage to pick

If you've never given regularly before, start at 0.5%. On a £35,000 salary that's £14.58 per month. You won't notice £14.58.

If you already give occasionally, aim for 1-2%. The Giving What We Can "Try Giving" pledge exists for exactly this: you commit to any percentage for any period. One percent for six months. Try it. If it's painless (and it almost certainly will be) you upgrade.

Their longitudinal data, published in 2023, shows that people who start with a fixed percentage almost never reduce it. The floor becomes the floor. What changes is the ceiling: as incomes rise, the amount grows automatically without any further decision required.

Three anchor points worth knowing. 0.5% is roughly £15/mo on a median UK salary, enough to make a real difference to one well-chosen charity. 1% is about £29/mo, enough to fully fund one child's mosquito net protection every month. 10% is the full Giving What We Can pledge. Most people reading this aren't there yet, and that's fine. The point is the habit, not the number.

Gift Aid does the heavy lifting

Do Gooder

One good decision a week

The research behind each piece takes hours. Get the next evidence-backed read every Tuesday, in 3 minutes.

Free weekly read. Unsubscribe anytime, no guilt.

If you're a UK taxpayer, your charity should be claiming Gift Aid on your donation. For every £1 you donate, HMRC adds 25p on top, at no cost to you. Higher-rate taxpayers can claim the remaining 20% back through their tax return too, effectively cutting your net donation cost by 40%.

Most people forget to tick the Gift Aid box. Some charities are bad at claiming it. When you set up your standing order, confirm with the charity that they're registered and that your donation is covered. Then check your bank statement in month two.

A £50/month standing order via Gift Aid is worth £62.50 to a registered UK charity. Over ten years that's £15,000 in charitable value from £12,000 of your money. The government is quietly matching 25% of your giving, and most donors either don't know or forget to activate it.

Choosing where the money goes

This deserves its own article (several exist on this site), but the short version: pick one charity you've evaluated, not five charities you feel vaguely positive about.

Splitting £30/month across six organisations means each gets £5. Admin costs alone eat a meaningful chunk of small donations. Better to give £30 to one organisation with strong evidence behind it.

GiveWell's top charity list remains the go-to starting point. Against Malaria Foundation costs roughly $5,500 per life saved. StrongMinds treats depression for under $500 per person. New Incentives costs around $900 per child fully vaccinated. These are auditable numbers backed by randomised trials, not marketing copy.

Pick one. Set up the standing order. Review once a year.

The identity angle

There's a psychological argument for giving regularly that doesn't get aired enough: it changes how you think about yourself.

CAF's 2022 research found that people who give by standing order are significantly more likely to describe themselves as "someone who gives" than people who donate equivalent amounts one-off. That self-description matters. It predicts future giving better than any other variable they measured.

You're not waiting to feel generous enough. You're a person who gives, and the standing order is the proof. Motivation follows the action, not the other way around.

What to do now

Log into your bank. Go to standing orders. Set up a new one:

- Payee: one well-evaluated charity (your choice, but make it real)

- Amount: 0.5-1% of your monthly take-home

- Start date: your next payday

- Frequency: monthly, indefinitely

Confirm Gift Aid if you're a UK taxpayer. Write down what percentage you've committed so you remember when you review it in a year. Then forget about it.

The direct debit does the work from here.

Sources used

- Giving What We Can longitudinal data on pledge retention (2023)

- Charities Aid Foundation "UK Giving Report" (2022, 2023)

- GiveWell cost-per-outcome estimates (2024 update)

- Behaviour change literature: Fogg Tiny Habits; Clear Atomic Habits habit stacking chapter

- HMRC Gift Aid statistics and eligibility rules (gov.uk)

- CAF standing order vs one-off donor lifetime value analysis

More in Small Acts