The giving-while-in-debt question

Rees Calder · 5 May 2026 · 7 min read

This is the question nobody in effective altruism wants to answer directly: should you give to charity when you're in debt?

The standard EA answer is some version of "it depends on your situation." Which is true and completely unhelpful. Here's a more honest framework.

The cold maths

Every pound of debt you carry has a cost. Credit card debt at 20% APR means £1,000 in unpaid balance costs you £200 per year in interest. That £200 is money you can never spend, invest, or donate. It evaporates.

If you donate £100 to the Against Malaria Foundation while carrying £1,000 of credit card debt, you're effectively borrowing £100 at 20% interest to make a charitable donation. The £100 donation saves approximately 0.02 lives (at GiveWell's $5,500 per life figure). Next year, the interest on your maintained debt costs you an extra £20 that could have funded more nets.

The breakeven question: At what interest rate does paying down debt become "better" than donating?

The answer depends on your counterfactual. If you would invest the money and donate later (patient philanthropy), stock market returns average 7-10% annually. Any debt costing more than 7-10% is destroying more value than investing would create. If you're comparing against donating now, the relevant number is harder to pin down, but the principle holds: high-interest debt is a guaranteed "negative return" that compounds against you.

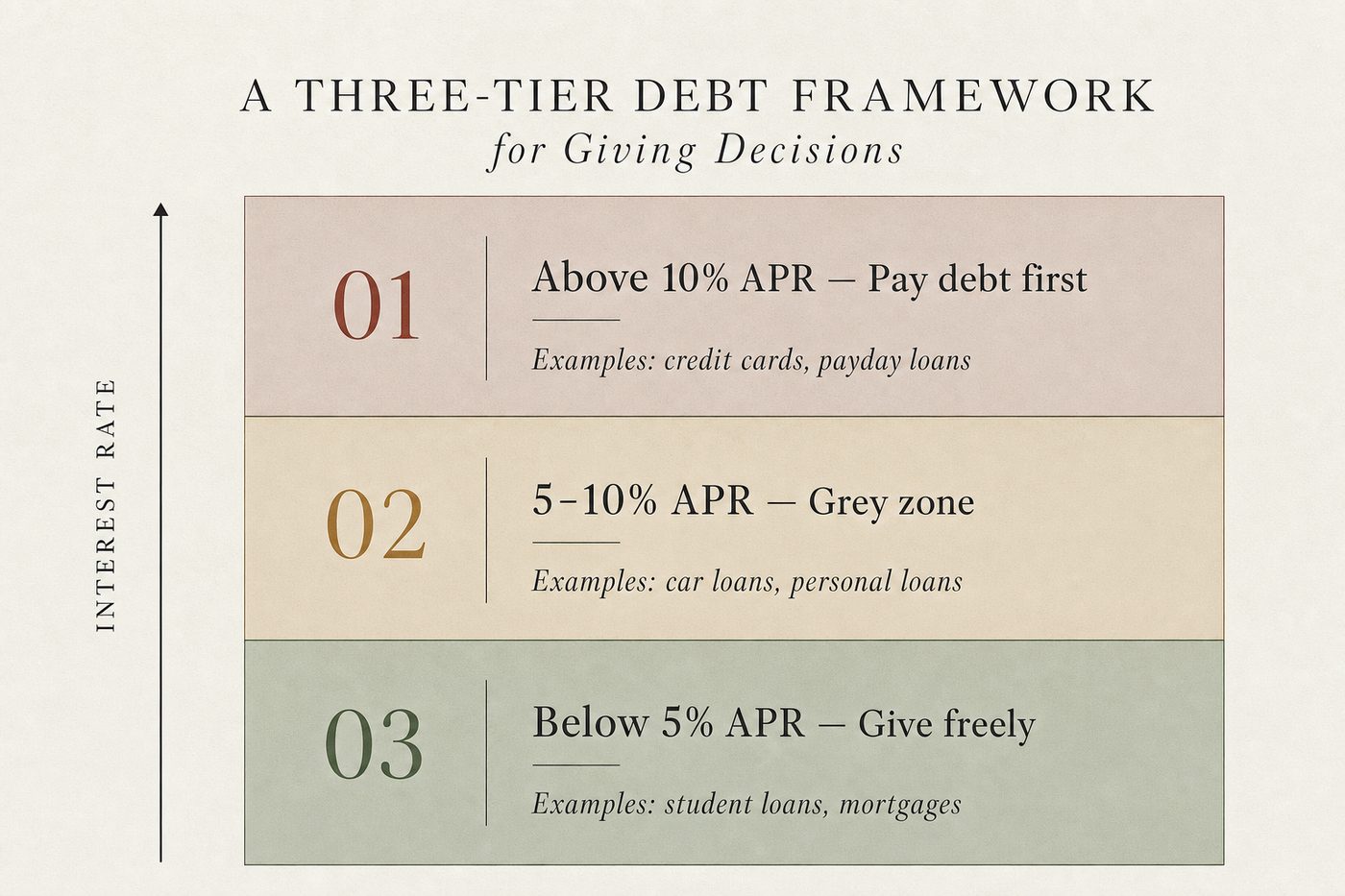

A practical framework

Tier 1: Debt above 10% APR (credit cards, payday loans, overdrafts). Pay this first. Full stop. The guaranteed 10-20% return of eliminating this debt exceeds almost any charitable investment you can make. Every pound going to credit card interest is a pound permanently removed from your lifetime capacity to do good. Getting to zero high-interest debt is the highest-return "donation" available to you.

Tier 2: Debt between 5-10% APR (car loans, personal loans). Grey zone. The maths are less decisive here. If maintaining a small giving habit (1-2% of income) preserves your identity as a giver and you'll scale up once the debt clears, the psychological value may justify continued giving. If every penny matters for debt payoff speed, redirect everything to the loan.

Tier 3: Debt below 5% APR (student loans, low-rate mortgages). This debt is rarely worth aggressive payoff. Student loans in the UK charge 4.3% (Plan 2) or effectively 0% if you never earn enough to repay in full before the 30-year write-off. A mortgage at 3-4% is the cheapest money you'll ever borrow. Giving while carrying this debt is entirely rational. The opportunity cost is low.

The exception: employer matches. If your employer matches charitable donations, the match changes the maths dramatically. A 1:1 employer match means your £100 donation creates £200 in charitable value. That's a 100% immediate return, which beats paying down any debt short of payday loans.

The psychological case for never fully stopping

Do Gooder

One good decision a week

The research behind each piece takes hours. Get the next evidence-backed read every Tuesday, in 3 minutes.

Free weekly read. Unsubscribe anytime, no guilt.

The maths above are clean but incomplete. They model humans as rational optimisers who will naturally restart giving once debt clears. They won't.

Identity maintenance. Research on habit formation (Lally et al., 2010) shows that once a habit breaks, restart friction is enormous. If you stop giving entirely during a debt payoff period that might last 3-7 years, the probability of restarting at meaningful levels is much lower than if you maintained even token giving throughout. A £10/month standing order to GiveWell during debt payoff preserves the identity of "someone who gives" at trivial financial cost.

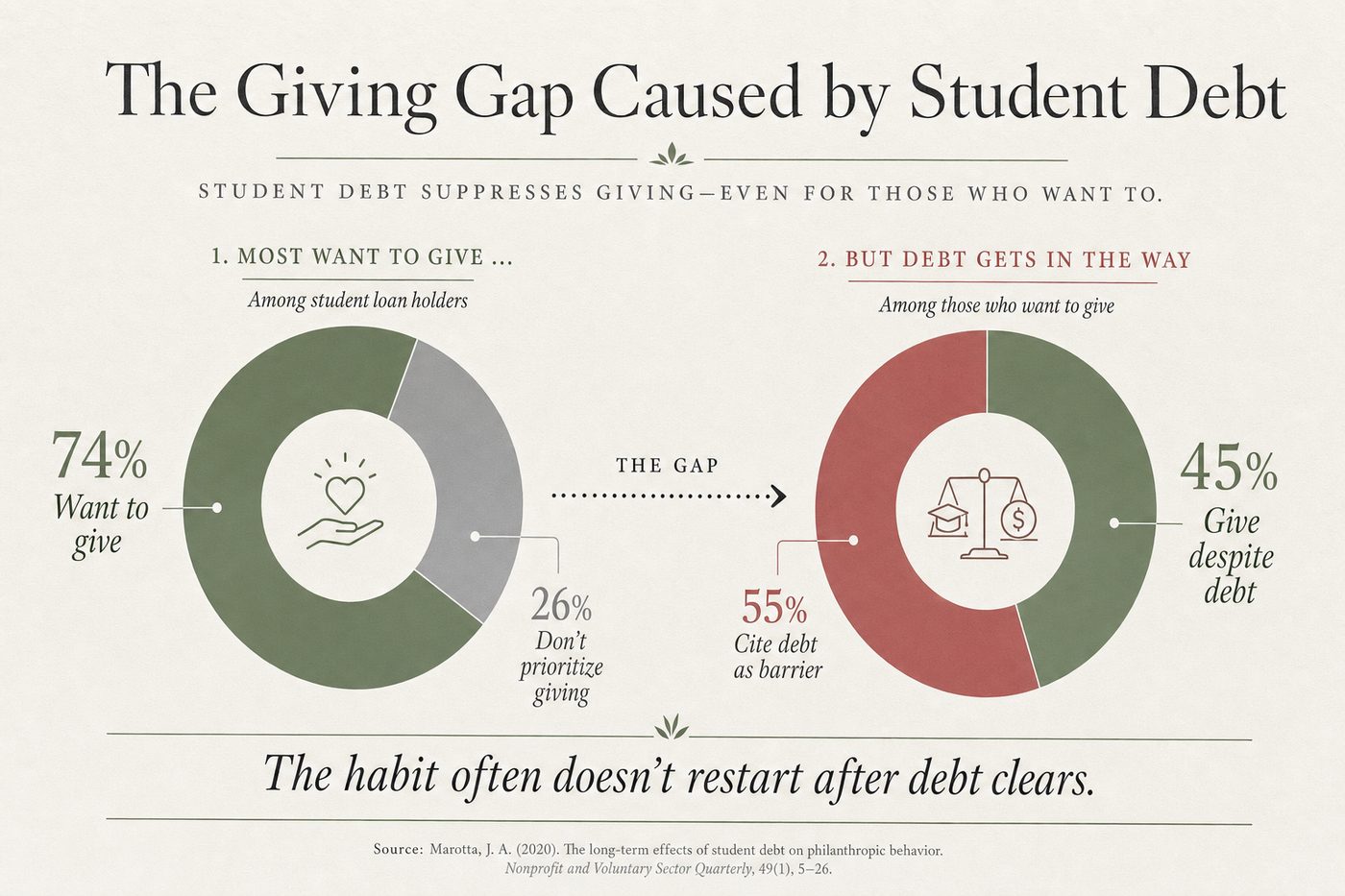

The survey data. Fidelity Charitable found that 74% of students surveyed have previously made charitable donations and consider giving important to them. Among those who stopped, 55% cited student debt as the primary reason. But the same survey found that giving often doesn't restart even years after debt clearance. The habit breaks and stays broken.

The GWWC Try Giving model. Giving What We Can's Try Giving pledge explicitly accommodates this: pledge any percentage for any period. 1% while in debt. 5% after debt clears. 10% once established. The structure acknowledges that life has seasons, and the goal is a trajectory, not a fixed point.

The patient philanthropy counter-argument

Phil Trammell (Oxford) makes a provocative case: if you invested £1,000 at 5% annual returns instead of donating it today, you'd have £125,000 in 100 years. The world of 2126 will have better knowledge about which interventions work, and your accumulated capital would fund vastly more good.

Applied to the debt question, this logic suggests: pay off debt first (guaranteed high return), then invest, then give when you have more to give and better information about where to direct it.

Why most people reject this. Open Philanthropy, the largest EA funder, explicitly rejects patient philanthropy because current giving opportunities are so good that waiting has high opportunity costs. GiveWell's top charities save lives today for $5,500 each. Waiting means real people die in the interim. The philosophical tension is genuine: do you optimise for total lifetime giving or for urgency of current need?

The resolution for most people. You're not deciding between "give now" and "give in 100 years." You're deciding between "give £50/month now while paying minimum on loans" and "throw everything at debt for 3 years then give £200/month forever." The second approach almost certainly produces more total giving and more total impact over a lifetime. The first approach preserves psychological continuity and addresses immediate suffering.

What to actually do

-

List all debts with interest rates. Anything above 10%: make aggressive payoff the priority. Redirect all discretionary spending including charitable giving until it's gone.

-

Keep a token giving habit. Even £5-20/month to a single evaluated charity. This is identity preservation, not impact maximisation. Accept that for this season.

-

Set a trigger. "When my highest-interest debt is below £X, I will increase giving to Y% of income." Write this down. Implementation intentions (Gollwitzer, 1999) are 2-3x more likely to be executed than vague goals.

-

Calculate your debt-free date. Use a compound interest calculator. Know exactly when you'll be free to give generously. That date is the start of your real giving career. Everything before it is the warm-up.

-

Don't feel guilty. Clearing high-interest debt is genuinely the most impactful financial decision most people in their twenties and thirties can make. Far from selfish, it's building the foundation for decades of effective giving.

Sources used

- Fidelity Charitable student giving survey (74% value giving, 55% cite debt as barrier)

- Phil Trammell "Discounting for Patient Philanthropists" (Oxford, working paper)

- 80,000 Hours "Why and how to earn to give" (earning-to-give framework)

- GiveWell cost-per-life estimates ($5,500, 2024)

- Lally, P. et al. (2010) "How are habits formed" European Journal of Social Psychology

- Gollwitzer, P. (1999) "Implementation intentions" American Psychologist

- GWWC Try Giving pledge structure (givingwhatwecan.org)

- Open Philanthropy position on patient philanthropy

More in The Life Edit